-

Equifax Canada data indicates COVID-19 financial crisis is not over for consumers, small businesses

来源: Nasdaq GlobeNewswire / 27 5月 2021 08:50:41 America/New_York

TORONTO, May 27, 2021 (GLOBE NEWSWIRE) -- Equifax Canada has released new data indicating that COVID-19 has had a varying impact on consumers and businesses. Many are hurting financially, whereas others have seen improvements to their financial standing.

On average consumers have seen their credit card balances decline during the pandemic and the lower debt levels have combined with fewer missed payments to generally boost credit scores. For businesses, however, decreased demand for credit presents a red flag most notably in the last three months of 2020. Credit inquiries dropped by over 60 per cent in the oil and gas sector, declined by 48 per cent in construction and retail activity fell 45 per cent.

“From a business perspective, data suggests that tough times will continue for small- to medium-sized enterprises,” said Rebecca Oakes, Equifax Canada’s AVP Advanced Analytics. “As with consumer credit, lower usage has led to commercial scores increasing slightly across Canada, but this isn’t necessarily a good thing. Businesses leverage commercial credit with suppliers as part of their day-to-day operations and therefore lower activity can indicate some early stress. Small businesses need to be spending money to be making money, and right now, they’re just not spending.”

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/7d2aebeb-7267-4a03-904e-07c70e9280c6

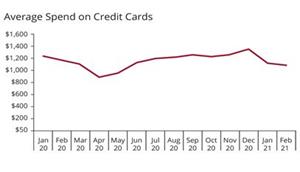

CREDIT CARD SPENDING RETURNING TO NORMAL LEVELS

Credit card performance is generally a good indication of consumers’ financial health. The lockdowns in early 2020 drove down credit card spending, which returned to normal levels by the end of the year. The fact that credit card balances have fallen indicates the impact of consumers paying off more of their debt. The government-benefit induced surge in disposable income has allowed 26 per cent more consumers to carry lower revolving balances in 2021. That reversed the trend prior to COVID, as credit card debt was growing quickly.The clean-up in consumers’ non-mortgage debt is evident in the overall performance with few people missing the monthly payments. The number of people that moved from being behind on payments to up-to-date (700k) outstripped those that started to miss payments (600k) in 2020. That reverses the trend in 2019 when those becoming delinquent (850k) exceeded those getting back on track (600k).

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/57ef0cdb-5da4-4ca2-9e5a-ab1173b92d1a

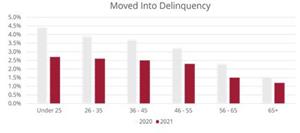

“Without question the pandemic has hurt the livelihood of many Canadians, but this new data offers some hope that many others have maintained if not improved their financial standing over last year,” added Oakes. “Government funding programs touching many corners of the economy will offer further assistance. On the credit side, however, the numbers do suggest more of a K-shaped recovery for younger consumers with some faring better than others.”

Missed payments and high use of revolving credit, like cards and lines of credit, are leading drivers on a consumer’s credit score. With these factors improving, 50 per cent of Canadians have reported higher credit scores over the past year. That compares to 45 per cent in 2019.

The improvement in credit conditions was most evident in the younger age groups. While they are traditionally more likely to miss payments, they posted the most significant improvement year-over-year. Similarly, their use of revolving credit also posted the most significant improvement compared to the pre-COVID period. This at least partially reflected the impact of programs like CERB and the significant reduction in frequent credit card transactions like gasoline, travel and restaurants.

“We expect recovery on the commercial side to remain uneven and sector driven,” said Oakes. “We’re watching this data very closely as small- to medium- sized businesses are incredibly important to the Canadian economy. Low-wage workers and young people are particularly impacted by current lockdown measures. We expect, however, that once businesses can re-open, this sector of the economy will rebound strongly, but the bounce back may not be consistent for all sectors.”

Equifax Canada will continue providing insights to assess the impact of the economic crisis while evaluating the impact of negative occurrences on business expansion. This is done through data and by applying a range of scores and indices to assess current and future business trends.

About Equifax

At Equifax (NYSE: EFX), we believe knowledge drives progress. As a global data, analytics, and technology company, we play an essential role in the global economy by helping financial institutions, companies, employers, and government agencies make critical decisions with greater confidence. Our unique blend of differentiated data, analytics, and cloud technology drives insights to power decisions to move people forward. Headquartered in Atlanta and supported by more than 11,000 employees worldwide, Equifax operates or has investments in 24 countries in North America, Central and South America, Europe, and the Asia Pacific region. For more information, visit Equifax.caMedia Contacts:

Andrew Findlater

SELECT Public Relations

afindlater@selectpr.ca

(647) 444-1197Tom Carroll

Equifax Canada

MediaRelationsCanada@equifax.com

(416) 227-5290

Average Spend on Credit Cards

The line graph charts the average spend on credit cards, which is returning to normal levels.

Moving into Delinquency

The bar graph indicates that credit conditions are improving across age groups.